Perhaps That’s No Longer the Right Question.

For decades, retirement planning was built around a deceptively simple idea: accumulate enough wealth during your working years, and eventually allow that wealth to replace your income.

The framework was straightforward >> Save consistently. Invest over time. Build a sufficiently large corpus. Retire.

For many investors, this approach worked well. But the environment around retirement has changed significantly.

Indians are living longer than previous generations, healthcare costs have become a larger financial consideration, and retirement is increasingly becoming a self-funded phase of life with nuclear families.

At the same time, retirement itself is evolving. Many individuals continue working beyond traditional retirement ages, not necessarily because they need to, but because they choose to. Others find themselves supporting multiple generations simultaneously, helping ageing parents while also providing support to adult children.

Against this backdrop, the familiar question: “How much do I need to retire?”, while important, is incomplete. The more meaningful question is: “Can my wealth continue supporting the life I have and want in the future?”

That distinction changes the way retirement planning needs to be approached.

The Limits of a Single Retirement Number

One of the most common ways investors think about retirement is through a target corpus.

Rules of thumb for target milestones such as 20x, 25x or 30x of expected annual retirement expenses are often used as starting points. These frameworks can provide useful direction, but they cannot capture the complexity of an individual’s retirement journey.

Retirement Changes the Role of Your Portfolio

A corpus does not exist in isolation. Its ability to support retirement depends on lifestyle choices, spending patterns, other income sources, investment strategy, healthcare requirements and legacy objectives.

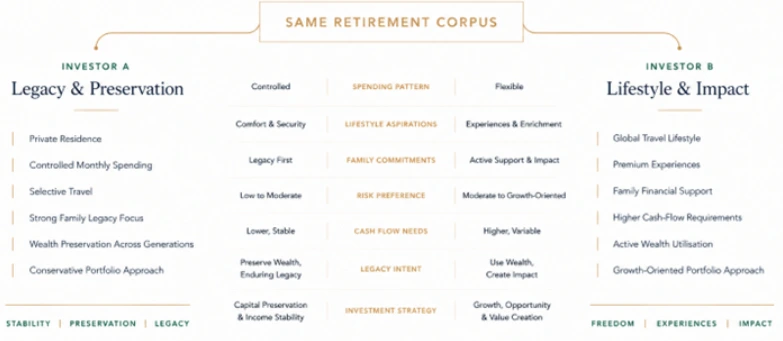

Consider two investors, both with a retirement corpus of ₹5 crore. The corpus will suffice or deplete very differently depending on the lifestyle of the retiree.

The investment journey changes significantly once retirement begins.

During the accumulation phase, investors benefit from regular savings, employment income and the ability to remain invested through market cycles. Market volatility, while uncomfortable, often creates opportunities to accumulate additional assets at attractive valuations.

Retirement reverses that relationship.

Instead of contributing to the portfolio, the investor begins depending on it. The portfolio is no longer simply a vehicle for wealth creation, it becomes a source of financial support.

Withdrawals become a regular requirement. Inflation gradually increases the cost of maintaining the same lifestyle. Healthcare expenses can arise unexpectedly. Market declines become more challenging because selling investments during periods of weakness can reduce the capital available to participate in future recoveries.

This is why retirement investing is not simply about generating the highest possible returns.

The objective shifts towards building a portfolio that can balance multiple priorities: generating sustainable income, preserving purchasing power, maintaining liquidity and remaining resilient through different market environments.

A portfolio that performs well in isolation may not necessarily be the portfolio that best supports a retiree’s financial goals.

Retirement Planning Is a Portfolio Construction Exercise

As investors accumulate greater wealth, retirement planning naturally becomes more.

A well-structured retirement portfolio typically needs to perform several roles simultaneously.

1. Generating Sustainable Income

For retirees, income planning becomes a central part of portfolio design.

Income may come from multiple sources, pensions, rental income, fixed-income investments, dividends or systematic withdrawals from investment portfolios. The challenge lies in coordinating these sources effectively while ensuring that withdrawals remain sustainable over time.

A well-designed income strategy considers not only current requirements but also how those requirements may evolve with inflation and changing circumstances.

2. Maintaining Growth and Purchasing Power

Retirement does not eliminate the need for growth.

With longer life expectancies, portfolios may need to support investors for several decades. Maintaining exposure to growth-oriented assets can help preserve purchasing power and protect against the impact of inflation over time.

The objective, however, is not aggressive growth at all costs. It is finding the right balance between growth potential and portfolio stability.

3. Managing Liquidity

Liquidity plays an important role in retirement planning.

Unexpected healthcare requirements, family commitments or large discretionary expenses can arise at any stage. Maintaining appropriate liquidity helps investors meet these needs without being forced to sell long-term investments during unfavourable market conditions.

Liquidity is therefore not simply idle capital, it is a tool for portfolio resilience.

4. Protecting Against Risks

A retirement strategy must also account for risks beyond market performance.

Adequate health insurance, contingency reserves and appropriate risk management measures can help prevent unexpected events from disrupting long-term financial plans.

Investment planning and risk protection need to work together.

5. Creating a Legacy

For many investors, retirement planning extends beyond supporting their own lifestyle.

It also involves determining how wealth should be transferred to future generations, supporting philanthropic objectives and ensuring that estate planning reflects their broader financial goals.

Legacy planning therefore becomes an important part of comprehensive wealth management.

A Retirement Portfolio Is More Than a Collection of Investments

Moving Beyond Products Towards Portfolio Solutions

One of the biggest shifts in wealth management today is that investors are becoming more focused on outcomes rather than individual products.

The conversation is increasingly moving towards questions such as:

- Can this portfolio continue generating income through market volatility?

- How much liquidity should be maintained?

- How should asset allocation evolve after retirement?

- How can wealth be structured efficiently across generations?

These are not product questions. They are portfolio construction questions.

A retirement strategy requires bringing together multiple elements: investments, cash flow planning, insurance, taxation, liquidity management and estate planning into a coordinated framework.

This is where a wealth management approach becomes valuable.

The right portfolio is not necessarily the one with the highest return potential in a favourable market environment. It is the one designed around the investor’s objectives and capable of adapting as those objectives evolve.

The Question Worth Asking

For today’s investors, the challenge is ensuring that wealth continues working effectively across changing markets, rising costs and evolving life goals.

A retirement corpus remains an important part of the equation. But it is only one part.

The more meaningful measure of retirement readiness is whether a portfolio has been structured to support the lifestyle it was built to fund.

At InCred Wealth, retirement planning begins with understanding an investor’s lifestyle, financial objectives and long-term priorities before designing a portfolio around them. Because successful retirement planning is not simply about reaching a number, it is about creating confidence that your wealth can continue supporting your goals over time.

Related Posts

India and the UK: More Than a Trade Agreement

Their significance is often revealed gradually, in investment decisions, supply…

Investors Who Outgrew Their Options

For years, the Indian investor's toolkit was elegantly simple: equity mutual…

Rupee at New Lows: Risk or Opportunity for Indian Investors?

The value of the Indian Rupee relative to the US Dollar is again in the…

How the Strait of Hormuz Impacts Oil Prices and Global Markets

In a digitally accelerated and financially sophisticated world, it is easy to…

What Makes a Landmass Strategically Valuable in the 21st Century?

In today’s interconnected world, the importance of global diversification…

Digital Transformation & Technology Adoption: How It’s Transforming the Indian Wealth Management Landscape

India’s wealth management landscape is in the middle of a profound shift. What…

India-UK Free Trade Agreement: A Strategic Leap for Growth & Investment

India and the United Kingdom have signed a historic Free Trade Agreement (FTA)…

Gold vs. Silver in 2025

2025 is turning out to be quite a challenging year for most investors and fund…